(Presentations were created using Wealthy and Wise®.)

Sometimes it seems there are only two kinds of prospects for long-term care insurance: Those who can’t afford it and more affluent candidates who can — but resist spending the money thinking, “I’ll just self-insure it.”

Next time you run across one of the latter, ask this question: “Would you like to know mathematically whether self-insuring is a valid option?” Most affluent people will want to hear what you have to say. For example:

Assumed Client Data

Clients: Age 65 and 60

Net Worth: $3.5 million

Desired After Tax Retirement Cash Flow: $100,000 indexed at 3.00%

Assumptions

- Assume a claim occurs in 8 years for one of the insureds that lasts for 6 years, after which death occurs.

- Assume the total benefits for the claim on a monthly basis will be $6,000 in today’s dollars — and medical inflation averages 5% a year.

- Assume the annual premium for a Long-Term Care policy with an inflation rider covering both individuals is $12,000 — reducing to $6,000 during the claim period.

- Assume the inflation rider increases total monthly benefits by 5% (compounded) a year.

- Assume retirement cash flow needs decline by 25% during and after the claim period.

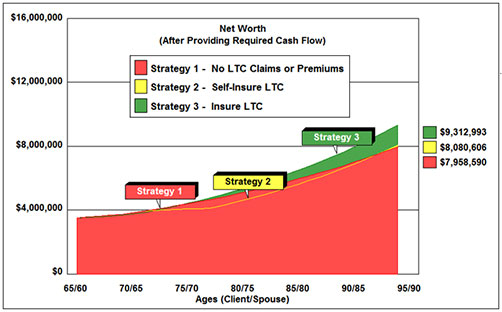

Let’s compare three scenarios:

- No coverage purchased and no claim costs assumed.

- No coverage purchased and claim costs paid via withdrawals from Net Worth.

- Coverage purchased and claim costs paid by the insurance company.

Hold on to your hats. Here are the results using InsMark’s Wealthy and Wise® software system.

Why is buying the LTC insurance the most efficient option?

Remember the assumption above where “retirement cash flow needs decline by 25% during and after the claim period”. Each client’s situation will require different assumptions, but in this case, it’s simple mathematics — the present value of the reduction in retirement cash flow more than offsets the present value of the cost of the premiums for the Long-Term Care policy.

This logic also makes self-insuring slightly more efficient than doing nothing — but the insurance option is the winning strategy by a large margin.

Go forth and be productive . . . but if you aren’t using Wealthy and Wise®, you don’t want to run into a competitor who is.

Click here to review the 20 summary reports for this Case Study.

Click here to review the 65 detailed reports for this Case Study.

InsMark’s Digital Workbook Files

If you would like some help creating customized versions of the presentations in this Blog for your clients, watch the video below on how to download and use InsMark’s Digital Workbook Files.

Digital Workbook Files For This Blog

Download all workbook files for all blogs

|

Note: If you are viewing this on a cell phone or tablet, the downloaded Workbook file won’t launch in your InsMark System. Please forward the Workbook where you can launch it on your PC where your InsMark System(s) are installed. |

InsMark’s Referral Resources

(Put our Illustration Experts to Work for Your Practice)

We created Referral Resources to deliver a “do-it-for-me” illustration service in a way that makes sense for your practice. You can utilize your choice of insurance company, there is no commission split, and you don’t have to change any current relationships. They are very familiar with running InsMark software.

Please mention my name when you talk to a Referral Resource as they have promised to take special care of my readers. My only request is this: if a Referral Resource helps you get the sale, place at least that case through them; otherwise, you will be taking unfair advantage of their generous offer to InsMark licensees.

Save time and get results with any InsMark illustration. Contact:

- Ben Nevejans, President of LifePro Financial Services in San Diego, CA.

Click here to learn more about InsMark’s Wealthy and Wise®. You can also contact Julie Nayeri at julien@insmark.com or 888-InsMark (467-6275). Institutional inquiries should be directed to David Grant, Senior Vice President – Sales, at dag@insmark.com or 925-543-0513.

![]()

Blog #5: It’s Awkward Trying to Sell My Friends

Blog #3: Identifying Good Prospects, Discarding Bad Ones

Blog #2: Anyone Want a Free Dog?

Blog #1: “Tell Me What’s Wrong With It?”

| 3 Reasons Why It’s Profitable For You To Share These |

| Blog Posts With Your Business Associates and |

| Professional Study Groups (i.e. “LinkedIn”) |

“Bob,

I’m enjoying your blogs. I’d like to request the two workbooks for blog # 6 (“How to Prove which of Your Clients Should Purchase Long-Term Care”).

Thanks for all the info.

John”

Hi John,

Since we released Blog #6, an update to Wealthy and Wise changed the results very slightly.

“Insure LTC” is still the winner by virtually the same wide margin.

“No LTC Claims or Premiums” moves to second place and “Self-insure LTC” drops to third.

Be sure you have the most current version of Wealthy and Wise. To check, click on Live Update under Help on the main menu bar of Workbook main window. If you see Wealthy and Wise checked, go ahead and Update; otherwise you’re good to go.

We’re glad you like the Blog, and we hope you recommend it to others. We’re already at almost 10,000 subscribers, and here’s an easy link to pass on:

Subscribe to Bob Ritter’s Blog.

Good luck and good selling.

The InsMark Team