(Click here for Blog Archive)

(Click here for Blog Index)

(Presentations in this Blog were created using InsMark’s Wealthy and Wise® and Loan-Based Split Dollar System using the Loan-Based Private Split Dollar module.)

|

In Part 1 of this series (Blog #159), we presented a Case Study in which Tom and Donna Anthony, ages 55 and 50, loan money to an intentionally defective irrevocable trust (IDIT) for the purpose of acquiring a survivor life insurance policy insuring their lives. The IDIT is a grantor trust formed on behalf of their children. The funding strategy is Loan-Based Private Split Dollar (LB-PSD), one of the modules in the InsMark Loan-Based Split Dollar System.

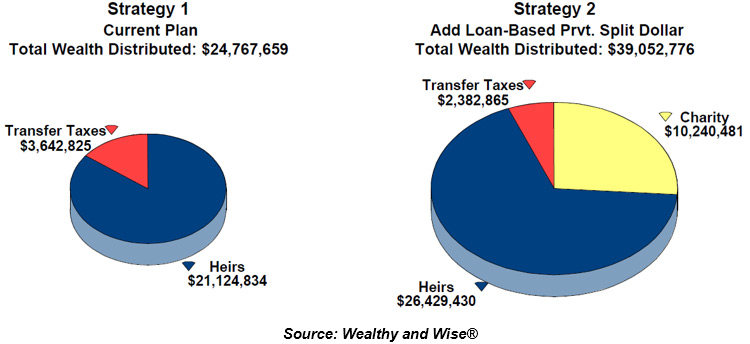

The results of the LB-PSD can be imported into our Wealthy and Wise® System where they can be integrated into the Anthony’s overall wealth management plan. Below are the comparative results of Strategy 1 (Ignore LB-PSD) vs. Strategy 2 (Include LB-PSD) where Strategy 2 also includes a significant charitable component in memory of Donna’s mother who passed away recently:

| Image 1 |

| Comparison of Alternatives at Ages 95/90 |

Total wealth distributed increases by over 157% (from $24,767,659 to $39,052,776).

Wealth to heirs increases by over 125% (from $21,124,834 to $26,429,430).

Transfer taxes reduce by over 35% (from $3,642,825 to $2,382,865).

Wealth to Charity goes from $0 to $10,240,481.

Note: If you have not reviewed Blog #159 to see how Strategy 2 was accomplished, I recommend you do so as not to miss the context of the LB-PSD variation discussed in this Blog.

Background

|

One of the key features of LB-PSD involves selecting the appropriate Applicable Federal Rate (AFR) used to establish the interest rate on the loans made to the trust by Tom and Donna. Click here for a report of the loans, AFRs, and planning alternatives that are the fundamental components of LB-PSD. (This report is the first page of the LB-PSD presentation in Blog #159.) While it is tempting to use the very low short-term AFR as the loan interest rate due by the trust (1.11% in April 2017, the date of the illustrations in Blog #159 and this Blog), in view of spiraling U.S. spending and the resulting deficit, I believe we will experience significant increases in all the AFRs over the next several years. Since the short-term rate must be renewed at least every three years, it is not advisable to use it as the selected loan interest rate in what appears to be an increasing interest rate environment. In Blog #159 and this Blog, the April 2017 long-term level rate of 2.82% is used for the 40-year life of the loans. |

|

An interesting feature of LB-PSD coupled with a grantor trust is that, in many cases, the AFR selected makes no practical difference which can make the selection of the long-term AFR a safe bet. Due to grantor trust rules, there is no income tax due by the lender on loan interest received from the trust, i.e., the lender and the trust are a single income tax entity. (IRC Section 671 and 675, IRS Reg. 1.671-2(c) and Rev. Rul. 85-13.) Since the trust’s only asset is the life insurance policy, Tom and Donna will make gifts to the trust to provide it with the cash flow to pay the loan interest. These gifts are returned as non-taxable loan interest creating a wash transaction. Unfortunately it can’t be deemed; a separate transaction by each party must be made.

With a life insurance policy bearing multiple premiums, each premium involves a new loan, and who knows what the AFR will be in future years? This tends to call for single premium policies except for their undesirable status as a modified endowment contract (MEC).

There is an alternative that solves both the unknown future AFR and MEC issues involving a feature of our LB-PSD called a Premium Reserve Account. It is funded with a one-time loan which avoids classifying the policy as a MEC by gradually feeding out funds for annual premiums. This also results in a lock-down of the long-term AFR for the entire length of the one-time loan with no risk of unknown future AFRs occurring*.

*For shorter terms of less than ten years, this strategy also works with the mid-term AFR.

Revised Illustrations

Click here to review the same survivor life policy featured in Blog #159 when funded with LB-PSD coupled with the Premium Reserve Account. The illustration date is the same as the LB-PSD in Blog #159, and the AFR used is the same for both. The Preface differs in Blog #161 due to an explanation of the Premium Reserve Account.

The next step is to export the values of this LB-PSD illustration to Source Data Storage. Wealthy and Wise has special receptors that recognize data from our LB-PSD illustrations. Click here to learn how to export data from LB-PSD to Wealthy and Wise.

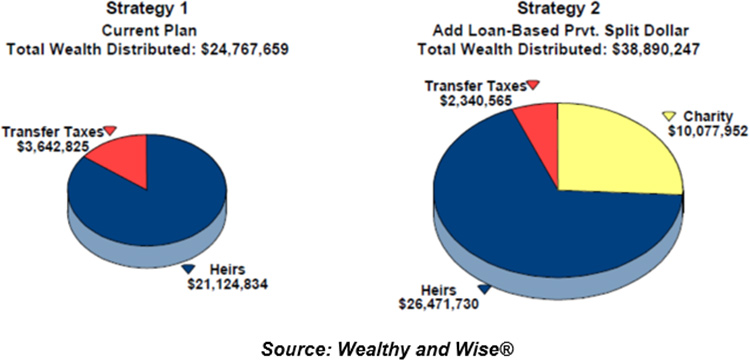

Wealthy and Wise Analysis

Below is the comparison between their current plan and an alternative with LB-PSD coupled with the Premium Reserve Account. It is virtually indistinguishable from Image 1 -- yet we have conquered the unknown future AFR issue and the MEC problem.

| Image 2 |

| Comparison of Alternatives at Ages 95/90 |

Like the pie chart above, the balance of the graphics in Blog #159 are a virtual mirror of those in Blog #161. If you are interested in understanding LB-PSD and haven’t studied Blog #159 in detail, you should. The purpose of the evaluation in this Blog is to show you how simple it is to avoid the two pitfalls of LB-PSD – unknown future AFRs and MEC status.

The gifts and loans associated with LB-PSD in Strategy 2 either in Blog #159 or this Blog produce a one-third decrease in Tom and Donna’s long-range net worth. That’s a lot of damage. To review what can be done to offset it, be certain to review Blog #159 starting right after Image 1. The solution includes an introduction to what we call Family Net Worth, and you don’t want to miss this vital new concept.

Final Thoughts

After using the Premium Reserve Account coupled with the long-term AFR, if the long-term AFR drops in future years, can the lower rate be substituted without penalty? There is nothing specific in tax law or regulation that provides for this, but click here for an authoritative report that makes the case for it.

One of the useful differences between LB-PSD and bank-funded premium financing is the AFR associated with LB-PSD is typically significantly lower than the rate charged by banks. In addition, most banks are unwilling to commit to premium financing loans of extended durations such as the loans associated with LB-PSD in Blogs #159 and #161. They are illustrated extending for 40 years and are presumed repaid from policy death benefits; however, there are sufficient policy cash values to support loans for an earlier repayment.

The extended duration of the loans mean that Tom and Donna must make gifts to the trust for loan interest every year into their 90s (and receive corresponding repayments from the trust for loan interest). Would this be a desirable detail at their older ages? Maybe not, but it can easily be alleviated by switching to accrued loan interest at some point, and there is plenty of cash value to support any such increase in the loan balance due. (The LB-PSD module can support this illustration variation.)

InsMark’s Digital Workbook Files

If you would like some help creating customized versions of the presentations in this Blog for your clients, watch the video below on how to download and use InsMark’s Digital Workbook Files.

New Zip File Downloaders

Watch the video.

Experienced Zip File Downloaders Download the zip file, open it, and double click the Workbook file name to open it in your InsMark System.

|

Note: If you are viewing this on a cell phone or tablet, the downloaded Workbook file won’t launch in your InsMark System. Please forward the Workbook where you can launch it on your PC where your InsMark System(s) are installed. |

If you obtain the digital workbook for Blog #161, Click here for a guide to its content.

Special plan documentation is required to support Loan-Based Private Split Dollar. InsMark’s Cloud-Based Documents On A Disk™ (“DOD”) contains a comprehensive set of specimen documents for it in the Wealth Transfer Plans section of documents. Look for Loan Regime Private Collateral Assignment Split Dollar in the Private Split Dollar Plans section of documents. If you are not licensed for DOD and would like more information, go to https://insmark.com/products/cloud-based-documents-disk. If you are licensed for DOD, you can access the document sets by signing in at www.insmark.com.

Special plan documentation is required to support Loan-Based Private Split Dollar. InsMark’s Cloud-Based Documents On A Disk™ (“DOD”) contains a comprehensive set of specimen documents for it in the Wealth Transfer Plans section of documents. Look for Loan Regime Private Collateral Assignment Split Dollar in the Private Split Dollar Plans section of documents. If you are not licensed for DOD and would like more information, go to https://insmark.com/products/cloud-based-documents-disk. If you are licensed for DOD, you can access the document sets by signing in at www.insmark.com.

Licensing InsMark Systems

To license any of the InsMark software products, visit our Product Center online or contact Julie Nayeri at Julien@insmark.com or 888-InsMark (467-6275). Institutional inquiries should be directed to David Grant, Senior Vice President — Sales, at dag@insmark.com or (925) 543-0513.

For help on how to use InsMark software, go to The Quickest Way To Learn InsMark.

Testimonials

“Bob Ritter is a master of illustrating complex issues in a simple easy to use manner that definitely helps you better serve your clients.”

Gary Curry, President and CEO, ORBA Insurance Services Inc., InsMark Platinum Power Producer®, Gold River, CA

“Major cases we are developing have all moved along successfully because of the sublime simplicity and communication capability of Wealthy and Wise. I guarantee that the proper use of this tool will dramatically raise the professional and personal self-image of any associate who dares to take the time to understand it . . .”

Phillip Barnhill, CLU, InsMark Gold Power Producer®, Minneapolis, MN

“The net worth and cash flow modeling that Wealthy and Wise provides is one of the best financial planning tools in the market place. In and of itself, it delivers tremendous value to the client. Moreover, when advisers update it annually, they deliver that tremendous value year after year. However, until advisers have sold themselves on the value proposition of charging fees, they will avoid them -- either to their financial detriment or in reduced service to clients. That is why advisers must be encouraged to believe the value they will create is worth far more than the fees they can charge.”

Mark Pace, CLU, RHU, ChFC, Creator of the Life Insurance Performance Management System, InsMark Gold Power Producer®, President, ObjectiView, Inc., Ridgeland, MS

“InsMark helps us help our clients understand their money and their choices. I always learn something new that changes what we do and how we can do it more efficiently. That translates to a better bottom line for us and for our clients. It’s making more money for everyone -- just by pushing InsMark buttons on the computer.”

Kay Corbin, CLU, ChFC, InsMark Platinum Power Producer®, Phoenix, AZ

Important Note #1: The hypothetical life insurance illustration associated with this Blog assumes the nonguaranteed values shown continue in all years. This is not likely, and actual results may be more or less favorable. Actual illustrations are not valid unless accompanied by a basic illustration from the issuing life insurance company.

Important Note #2: Many of you are rightly concerned about the potential tax bomb in life insurance that can accidentally be triggered by a careless policyowner. Click here to read Blog #51: Avoiding the Tax Bomb in Life Insurance.

Important Note #3: The information in this Blog is for educational purposes only. In all cases, the approval of a client’s legal and tax advisers must be secured regarding the implementation or modification of any planning technique as well as the applicability and consequences of new cases, rulings, or legislation upon existing or impending plans.

“InsMark” and “Wealthy and Wise” are registered trademarks of InsMark, Inc.

“Documents On A Disk” is a trademark of InsMark, Inc.