(Click here for Blog Archive)

(Click here for Blog Index)

(Presentations in this blog were created using Wealthy and Wise ® and the Leveraged Compensation System)

|

-Look-Alike-meets-the-calculation-dynamics-of-Wealthy-and-Wise-(part-2-of-2)-769x513.jpg)

|

Be sure you have read Blog #191: 401(k) Look-Alike (Part 1 of 2) before proceeding with this Blog. The material below assimilates the executive’s share of the data from that analysis into InsMark’s Wealthy and Wise. The purpose is to generate a Do-it vs. Don’t-do-it™ evaluation integrated within a client’s pre-existing retirement plan to measure the effectiveness of the 401(k) Look-Alike strategy. It is essential for you to understand the mechanics of the 401(k) Look-Alike before proceeding, thus the recommendation that you read Blog #191 if you haven’t already done so. |

As described in Blog #191, the 401(k) Look-Alike provides a significant benefit for Tony Jamison, age 45, President/CEO of Jamison Advertising, Inc. Let’s see how it integrates with a retirement plan for Tony and his wife, Allison, also age 45.

| Current Net Worth |

| Tony and Allison Jamison |

| 1 | Continuing contributions of $19,000 increasing by 2.00% a year with a 25% match by the employer. |

Click here for comments regarding yields, sequence of returns, and Monte Carlo simulations.

Retirement Cash Flow Goal

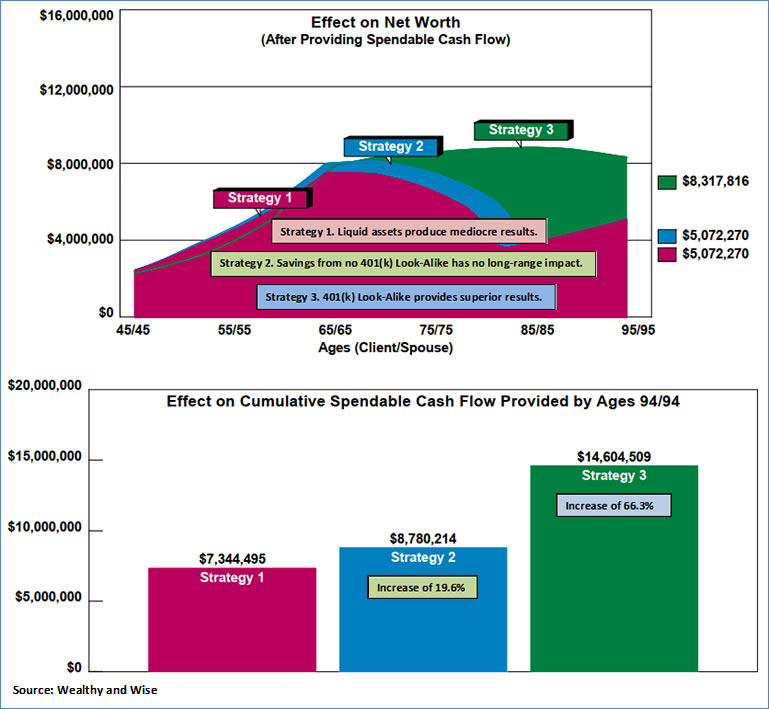

Tony and Allison would like to have $30,000 a month in after-tax, retirement cash flow starting at age 65 including a 2.00% cost of living assumption. Extending the analysis to their age 95 requires $10,800,000 of cumulative, after-tax cash flow ($30,000 x 12 months x 30 years). The 2.00% indexing increases the total cash flow to $14,604,509 between ages 65 and 95 – five years past their joint life expectancy. (Joint life expectancy indicates that at least one spouse is presumed to be alive.)

Let’s manage this objective as follows:

Strategy 1: Current liquid assets supply the cash flow.

Strategy 2: The 401(k) Look-Alike requires Tony to reduce his compensation by $100,000 a year for seven years costing him $55,000 each year in their combined 45% federal and state income tax bracket. If he does not participate, that $55,000 can be added to their investments for seven years with 25% ($13,750) going to their tax-exempt account and 75% ($41,250) directed to their equity account.2

Strategy 3: Tony enters into the 401(k) Look-Alike arrangement.

| 2 | Based on their customized reinvestment options for excess cash flow programmed in their Wealthy and Wise analysis. (See the Excess Cash Flow and Reinvestment Options sub-tab located on the Illustration Details tab in Wealthy and Wise.) |

Below is the comparison of the three Strategies:

| Image 1 |

| Net Worth Evaluation |

| for |

| Tony and Allison Jamison |

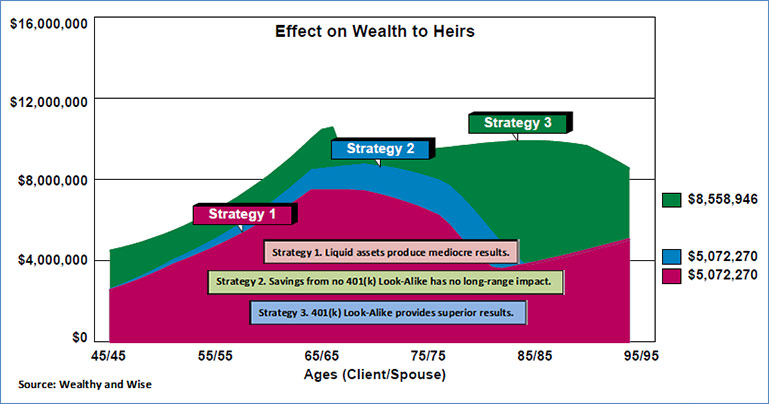

The results are significantly in favor of the 401(k) Look-Alike as their long-range net worth is 64% greater than either alternative. Strategy 2 shows a slight increase in spendable cash flow, but it is Strategy 3 that fulfills Tony and Allison’s goal of $30,000 a month of after-tax cash flow from age 65 – 95 indexed at 2.00%.

The worst aspect of Strategy 1 is that from age 82 forward, there is no retirement cash flow at all as the only remaining assets are illiquid. The same is true for Strategy 2, starting at age 85.

| Image 2 |

| Wealth to Heirs Evaluation |

| for |

| Tony and Allison Jamison |

Note: To produce more cash for investment at the point cash flow is depleted, they could sell their primary residence and move to their vacation home; however, this would add only three additional years of cash flow at their desired level. (See “Sale of principal residence” on the Illiquid Asset tab in Wealthy and Wise.) An alternative – weak for this example – would be to consider a reverse mortgage, but that is a subject for another Blog.

Click here to view a two-page report of the year-by-year numbers of the three Strategies.

Click here to review a reduced series of reports for the entire evaluation.

Click here to review all the Wealthy and Wise output associated with this Blog. This analysis contains 52 numerical reports and several graphics totaling 106 pages. That is a large number; however, with a Wealthy and Wise evaluation, I recommend you have all applicable reports for a given case with you when visiting with a client or client’s attorney or CPA. Wealthy and Wise backs up every number shown, and you never know which report you’ll need to answer the inevitable question, “Where did this number come from?”

Many Wealthy and Wise users select a few key illustrations in a central section (I did this with the reduced series of reports above), and put the balance in an Appendix. (I did not add an Appendix above.) You can create a more elaborate report organization (e.g., Table of Contents and Section pages) by selecting the following prompt available at the bottom right of the Main Workbook Window of Wealthy and Wise:

Conclusion

Most executive benefits specialists do not take the extra step of integrating their particular product with each executive’s retirement plan. As you have seen above, there are significant reasons to do so. Frankly, it turns each executive into a long-range client rather than a benefit participant.

I still maintain a close relationship with many clients from my personal-production days, and I have introduced many of them to Wealthy and Wise since InsMark developed it in the early 1990s. (Early name: InsGift). Most cases involve monitoring fees. I often get calls asking if I will run some new financial issue through Wealthy and Wise to gauge its effectiveness for them. How many calls like that do you receive? It is another example of why charging monitoring fees makes such good sense.

Blog #97 was a guest Blog by Mark Pace, CLU, RHU, ChFC, President, ObjectiView, Inc. that had superb logic regarding charging fees. It was followed up by Blog #98 that involved a Case Study in which monitoring fees were included in a Wealthy and Wise analysis. You might find both Blogs useful to your practice.

Specimen Documents

Documentation for a 401(k) Look-Alike is different from any other split dollar arrangement. Specimen installation documentation for 401(k) Look-Alike is available in InsMark’s Cloud-Based Documents On A Disk™ (DOD) in both the Business Owner Benefit Plans and the Key Employee Benefit Plans section of documents. These specimen documents don’t exist anywhere else, so if you use this concept, you will need them – particularly those relating to severance. If licensed for DOD, you can access these documents from within the 401(k) Look-Alike module (part of the Leveraged Compensation System) by clicking on this section on the lower right of the screen in edit mode:

Documentation for a 401(k) Look-Alike is different from any other split dollar arrangement. Specimen installation documentation for 401(k) Look-Alike is available in InsMark’s Cloud-Based Documents On A Disk™ (DOD) in both the Business Owner Benefit Plans and the Key Employee Benefit Plans section of documents. These specimen documents don’t exist anywhere else, so if you use this concept, you will need them – particularly those relating to severance. If licensed for DOD, you can access these documents from within the 401(k) Look-Alike module (part of the Leveraged Compensation System) by clicking on this section on the lower right of the screen in edit mode:

Alternatively, assuming you are appropriately licensed, you can access the documents directly by logging into My InsMark at this address and look for (My InsMark) upper right side: https://www.insmark.com/.

Licensing InsMark Systems

For licensing information regarding the Wealthy and Wise, the Leveraged Compensation System (where 401(k) Look-Alike is located) and Cloud-Based Documents On A Disk™, contact Julie Nayeri at Julien@insmark.com or 888-InsMark (467-6275). Institutional inquiries should be directed to David Grant, Senior Vice President — Sales, at dag@insmark.com or (925) 543-0513.

For those who would like a discounted suite of our entire product line, visit our Platinum Power Producer site.

To license any other InsMark software product, visit our Product Center online or contact Julie Nayeri at Julien@insmark.com or 888-InsMark (467-6275). Institutional inquiries should be directed to David Grant, Senior Vice President — Sales, at dag@insmark.com or (925) 543-0513.

For help on how to use InsMark software, go to The Quickest Way To Learn InsMark.

InsMark’s Digital Workbook Files

If you would like some help creating customized versions of the presentations in this Blog for your clients, watch the video below on how to download and use InsMark’s Digital Workbook Files.

If you would like highly qualified design assistance with no commission split required, contact LifePro Financial, InsMark’s Referral Resource discussed below.

New Zip File Downloaders

Watch the video.

Experienced Zip File Downloaders Download the zip file, open it, and double click the Workbook file name to open it in your InsMark System.

|

Note: If you are viewing this on a cell phone or tablet, the downloaded Workbook file won’t launch in your InsMark System. Please forward it to your PC where your InsMark System(s) are installed. |

If you obtain the digital workbook for Blog #192, click here for a guide to its content. It will be invaluable to you.

Testimonials

“Thanks to the genius of Bob Ritter and InsMark, I was able to complete two cases in the last few months using the 401(k) Look-Alike module in the InsMark Leveraged Compensation System. Annual premiums total was over $90,000. Before reaching out to Bob, I struggled with conceptualizing and communicating this new deferred compensation logic to the business owners and their key employees. With the InsMark software, the compelling case logic was immediately obvious to everyone. In addition, the software is easy to learn and use. InsMark continues to work magic for me and my business!”

Glenn A. Main III, InsMark Power Producer, The Main Point LP, Pittsburgh, PA

“InsMark has created without question the best suite of software for our industry that has ever existed. I personally have been using their software for almost 30 years, and it changed my career. This unique and user friendly software will add many thousands to your income for as long as you’re in business. InsMark makes me look good, and it will you as well.”

Simon Singer, CFP®, CAP®, RFC®, Past President International Forum, InsMark Platinum Power Producer®, Encino, CA

“InsMark is the Picasso of the financial services world — their marketing savvy never fails to amaze me.”

Doug Peete, Past President, Top of the Table, and InsMark Power Producer, Overland Park, KS

“The reason I use InsMark products is because they are so good at explaining financial concepts to all three parties: 1) the producer trying to explain the idea; 2) the computer technician trying to illustrate it; 3) the customer trying to understand it.”

Rich Linsday, CLU, AEP, ChFC, InsMark Platinum Power Producer®, Top of the Table, International Forum, Pasadena, CA

“InsMark has increased my production by 10 fold. It clearly communicates to the client the best financial scenario to take.”

Gary Sipos, M.B.A., A.I.F.® InsMark Platinum Power Producer®, Sipos Insurance Services, Freehold, NJ

“InsMark” and “Wealthy and Wise” are registered trademark of InsMark, Inc.

“Cloud-Based Documents On A Disk” is a trademark of InsMark, Inc.

Copyright © 2019 InsMark, Inc.

All Rights Reserved

Important Note #1: The hypothetical life insurance illustrations and alternative investments referred to in this report assume the nonguaranteed values shown continue in all years. This is not likely, and actual results may be more or less favorable. Actual illustrations of life insurance are not valid unless accompanied by a basic illustration from the issuing life insurance company.

Important Note #2: The information in this Blog is for educational purposes only. In all cases, the approval of a client’s legal and tax advisers must be secured regarding the implementation or modification of any planning technique as well as the applicability and consequences of new cases, rulings, or legislation upon existing or impending plans.

Important Note #3: Many of you are rightly concerned about the potential tax bomb in life insurance that can accidentally be triggered by a careless policyowner when policy loans are present and net cash values are so low that the income tax on the gain on surrender (calculated using gross cash values less basis) is more – often significantly more – than the net cash surrender value.

This lurking tax bomb can be present in all forms of whole life and universal life where policy loans of any type are utilized. It can be avoided, and you, the producer, are key to making sure your clients are aware of how to sidestep it.

A tax bomb can be avoided if the policy is neither surrendered nor allowed to lapse, since the policy death benefit wipes away the income tax liability. The foundation of this special treatment is IRC Section 101. This statute provides that the proceeds of life insurance maturing as a death claim are exempt from federal income tax. This applies to the full death benefit, including any cash value component whether loans exist or not.

Can your clients remember these facts years into the future? If they are incapacitated, will family members understand the issues? It is probably best to file a short note with the policy – something like this (although your compliance officer will likely have preferred language):

If/when you take policy loans on this policy, be sure to talk to your financial adviser before surrendering or lapsing the policy in order to anticipate unexpected tax consequences that may otherwise be avoided.

Some life insurance companies have concierge units that monitor loan status at the point of lapse or surrender, and you would be well-advised to select an insurance company with this capacity. To be effective regarding the tax bomb, such carriers need to be proactive in their client relationships, not merely reactive to client inquiries. I hope that ultimately the policyholder service division of all life insurance companies will bring this potential liability to the attention of those surrendering or lapsing policies, particularly those policies with 50% or more of the gross cash value subject to outstanding loans.