(Click here for Blog Archive)

(Click here for Blog Index)

(Presentations in this blog were created using the InsMark® Illustration System)

This Blog brings you InsMark’s best analytics for helping your clients determine which is the best life insurance for them to consider. “Best policy for my client” cannot be established by a standard that applies to all clients. Rather, it must be determined by an objective analysis that is unique to each client as to the type of policy as well as each client’s personal comfort with different levels of death benefit, cash value, cash flow, and interest or dividend assumptions.

A new InsMark innovation helps you establish rational reasons why a specific life insurance policy is selected as suitable for a client. This logic is established using the InsMark Compare™ module in the InsMark Illustration System. This module uses numbers, percentages, and graphics to compare up to four different policy illustrations as to premiums, cash values, death benefits and, if included, after-tax cash flow.

As part of InsMark’s Prudent Care, we also used Various Financial Alternatives in the InsMark Illustration System for a comparison of each policy’s differences. A portion of the comparison also discloses and compares Plan Costs: the taxes and charges of each alternative investment contrasted with the internal administrative fees and mortality charges of the life insurance.

The overall evaluation confirms that Prudent Care™ helps guide your client’s selection of the most suitable life insurance policy.

InsMark Compare™

This module compares up top four different life insurance illustrations on one page—both numerically and graphically.

The InsMark Compare™ illustration module in the InsMark Illustration System also contains an optional FINRA-approved Risk Questionnaire which helps clients self-identify their personal risk profile. The Questionnaire is provided courtesy of Back Room Technician (BRT) by Advisys, Inc. You don’t need to be licensed for BRT to use the Questionnaire; however, you should be certain that your compliance department approves its use. (If you aren’t licensed for Back Room Technician, you are missing a terrific piece of software.)

Many of you have your own suitability procedures, and I am not suggesting you abandon them; rather, we are providing the BRT variation for you to consider as a coordinated part of InsMark Compare™.

Click here to review the FINRA-approved Risk Questionnaire with Scoring.pdf.

Case Study

Jack Hudson, age 45, is considering purchasing an indexed universal life policy (“IUL”) with substantial after-tax cash flow during retirement years. Please review the data that follows assuming that Jack and his wife, Amy, are your potential clients.

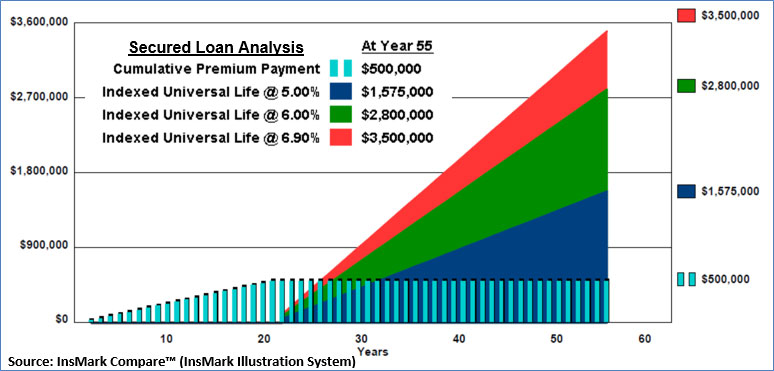

Assume as part of your educational responsibilities that you have prepared a presentation featuring different life insurance strategies using the InsMark Compare™ module in the InsMark Illustration System. Below is a graphic of the comparative, after-tax, cash flow results during retirement of the same IUL policy illustrated at three different interest assumptions (5.00%, 6.00%, and 6.90%). It provides you with an impressive start of your presentation, which you could introduce by saying, “Let’s begin our meeting with my analysis of the policy that I think you should consider.”

| Image 1 |

| InsMark Compare™ Policy Loan Analysis |

| Various Results of Indexed Universal Life |

| Using Different Interest Assumptions of |

| 5.00%, 6.00%, and 6.90% |

Click here to review the entire illustration format.

InsMark Compare™ can be a very effective illustration. You can use it to evaluate the same policy from different carriers or different policies from different carriers, i.e., whole life, universal life, indexed universal life, and variable universal life. You can designate each one as either conservative, moderately conservative, moderate, moderately aggressive, or aggressive. Be careful with these designations as it is tempting to exaggerate one way or the other based on your personal preferences.

Various Financial Alternatives

Since the beginning days of the InsMark in 1982, we have believed that clients make better decisions when comparing recommendations to other alternatives. It is better to do this with them than their doing it by themselves — or worse, doing it with someone else who is not particularly open-minded about life insurance.

Your client’s perception of suitability—perhaps different than yours—can make a huge difference in your presentation. InsMark Compare can quickly determine your client’s position on suitability.

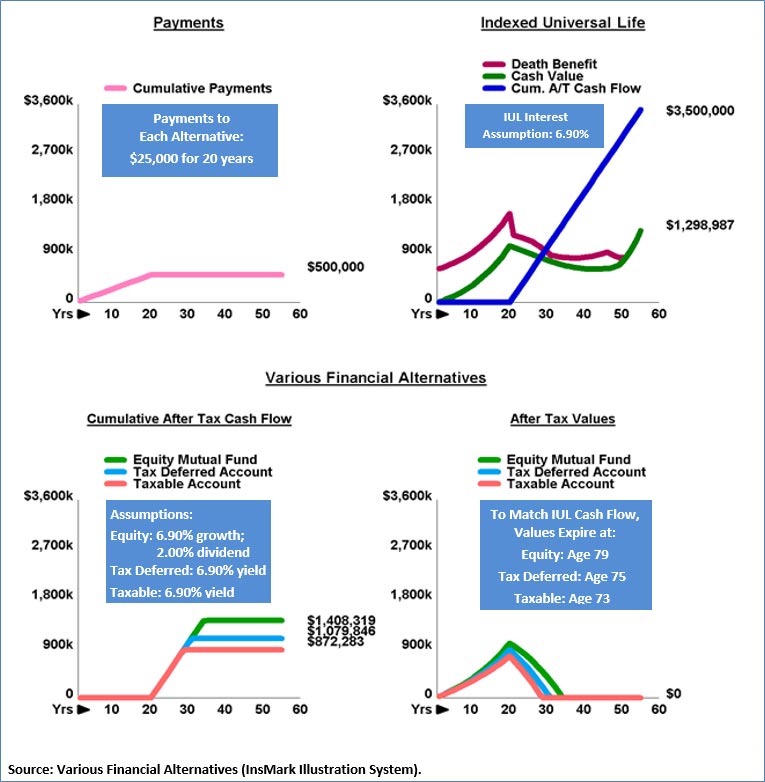

Let’s assume Jack and Amy believe that Indexed Universal Life @ 6.90% (“Moderately Aggressive”) as presented in the InsMark Compare™ illustrations, is a satisfactory assumption.

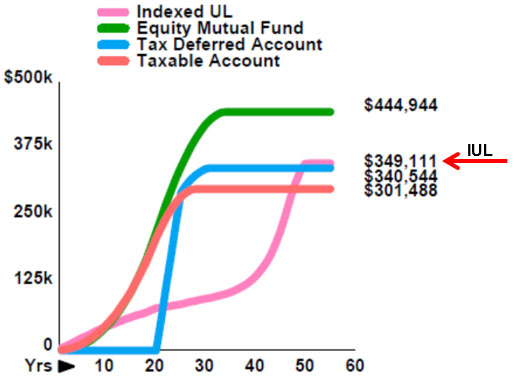

Below is a graphic of the second evaluation, Various Financial Alternatives.

| Image 2 |

| Three Hypothetical Financial Alternatives |

| Taxable, Tax Deferred, and Equity Mutual Fund |

| Compared to Indexed Universal Life |

| with an Interest Assumption of 6.90% |

Unfortunately, the illustrated Alternatives produce a classic case of running out of money in retirement: the taxable account at Jack’s age 73; the tax deferred account at Jack’s age 75; and the equity fund at Jack’s age 79. The illustrated IUL does not run out of money.

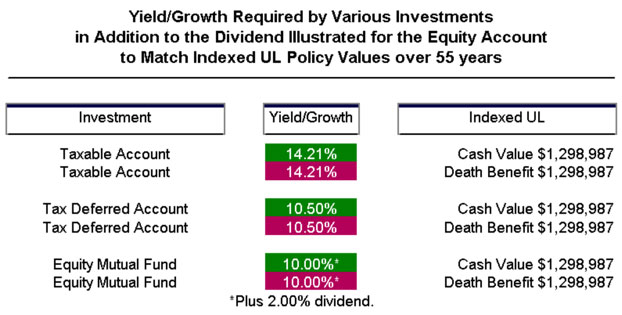

The following image is a vital part of the presentation that compares the necessary yield/growth of the alternatives with the Indexed Universal Life at 6.90%:

| In Order to Match the Indexed Universal Life |

| The taxable account must earn 14.21% (731 basis points more than the IUL); |

| The tax deferred account must earn 10.50% (360 basis points more than the IUL); |

| The equity account must have growth of 10.00% plus the 2.00% dividend |

| (510 basis points more than the IUL). |

Some clients will express disbelief that IUL has such an advantage.

Here are the core reasons why IUL performs better:

- Unlike the Alternatives, the values of the IUL grow tax-free and are distributed tax free (via secured loans).

- Unlike the Alternatives, the loans are automatically repaid at death on a tax free basis from the policy death benefit.

- Unlike the Alternatives, IUL cash value does not decrease due to down-markets; however, it increases with up-markets. This a significant advantage in years like 2020 with extensive gyrations in the stock market. (Imagine every time the market drops, your IUL cash value is unaffected; every time it recovers, it can impact your cash value favorably.

- Unlike the Alternatives, tax-free cash flow (secured loans) from the IUL experiences automatic enhancement due to the availability of participating loans. This unusual feature ensures that policy values securing such loans participate in the same stock index credited to non-loaned cash values. Read my Blog #52 for a discussion of participating loans.

- Plan Costs: Unlike the Alternatives with hefty tax and internal costs, the IUL’s cumulative costs are substantially less, part of the reason it performs so well.

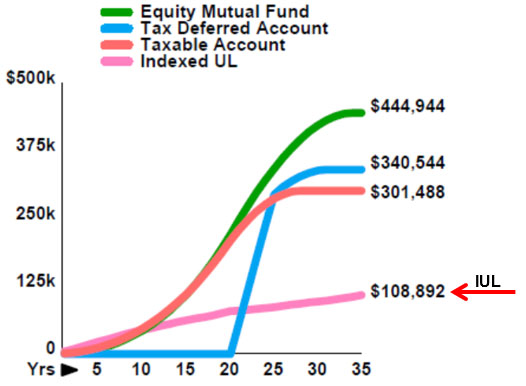

Note: During the first nine years, cumulative Plan Costs are more for the IUL, and this is where both Suze Orman and Dave Ramsey typically center their objections to cash value life insurance. Starting in year 11, and every year after that, all the Alternatives surge well past the IUL, as you can see in the graphic that follows. This should take care of Suze’s and Dave’s criticism.

Comparison of Plan Costs

Below are two graphics from the Various Financial Alternatives module comparing the Plan Costs of the Alternatives to the recommended IUL. The first graphic compares cumulative Plan Costs in the last year that the best performing Alternative, the equity fund, retains any value (Jack’s age 79; Year 35).

| Image 3 |

| Comparison of Plan Costs |

| (Jack’s age 79; Year 35) |

Below is the Plan Cost comparison extended to age 100. The IUL still retains values and produces cash flow. Its Plan Costs have continued to rise—a small price to pay as the other alternatives have each crashed and burned years earlier.

| Image 4 |

| Comparison of Plan Costs |

| (Jack’s age 100; Year 55) |

Plan Costs are impressively in favor of IUL, and this is one of the core reasons for its superior results.

Click here to review both proposals in one illustration format organized as follows:

- Pages 1 through 7: InsMark Compare™ illustrations.

- Pages 8 through 19: Various Financial Alternatives (main illustration pages including Plan Costs).

- Pages 20 through 37: An Appendix (with several backup pages detailing calculations featured in Various Financial Alternatives).

Conclusion

This Blog is InsMark’s best effort to provide you with a presentation sequence that is impressive, convincing, and quickly closed — and I hope it is useful to you.

The only missing feature is a comparison to “buy term and invest the difference.” I will feature that comparison in Blog #200 scheduled for April.

Your Comments

What are your thoughts and conclusions after reviewing this material? Please add your comments to this Blog. Your email address will not be published.

Illustration Suggestions

You can create all-proposals-in-one-illustration by using this prompt on the Workbook Main Window of the InsMark Illustration System: If you download the InsMark Illustration System digital Workbook file for Blog #199 available below, there is a Notes section at the bottom of the Workbook Main Window with some text to help you prepare all-proposals-in-one-illustration.

You can create all-proposals-in-one-illustration by using this prompt on the Workbook Main Window of the InsMark Illustration System: If you download the InsMark Illustration System digital Workbook file for Blog #199 available below, there is a Notes section at the bottom of the Workbook Main Window with some text to help you prepare all-proposals-in-one-illustration.

Life Expectancy

Jack’s life expectancy at his current age of 45 is 83. His and Amy’s joint life expectancy is age 90, which means one of them, on average, should remain alive after 90.

Why did I illustrate this Case Study to age 100? Because there are more centenarians living today than ever before. There are estimated to be 80,000 U.S. centenarians in 2019, a figure expected to grow to about 3,676,000 in 2050, according to a recent report by Pew Research Center, the Washington D.C.-based think tank.

A critical aspect of IUL is that it can remain in force to age 120 for the rare person who lives anywhere near that long.* If death occurs before that, the unique tax-free dollars of death benefit are present for beneficiaries—eliminating any deferred income tax inherent in the policy loan aspect of the transaction. The foundation of this particular treatment is IRC Section 101 that provides the proceeds of life insurance maturing as a death claim are exempt from federal income tax. This advantage applies to the full death benefit, including any cash value component, whether loans exist or not.

*According to Wikipedia, List of American supercentenarians, as of March 24, 2020, the Gerontology Research Group (GRG) lists the oldest living American as Hester Ford (born in Lancaster, South Carolina, August 15, 1905), aged 114 years, 222 days. The longest-lived person ever from the United States was Sarah Knauss, of Hollywood, Pennsylvania, who died on December 30, 1999, aged 119 years, 97 days.

Licensing

To reproduce your versions of the illustrations and graphics in this Blog, license the InsMark Illustration System by contacting Julie Nayeri at julien@insmark.com or 888-InsMark (467-6275). You can also license it at insmark.com. Institutional inquiries should be directed to David Grant, Senior Vice President – Sales, at dag@insmark.com or (925) 543-0513.

InsMark’s Digital Workbook Files

If you would like some help creating customized versions of the presentations in this Blog for your clients, watch the video below on how to download and use InsMark’s Digital Workbook Files.

If you would like highly qualified, illustration design assistance with no commission split required, contact LifePro Financial, InsMark’s Referral Resource, discussed below.

Digital Workbook Files For This Blog

New Zip File Downloaders

Watch the video.

Digital Workbook Files For This Blog

Experienced Zip File Downloaders Download the zip file, open it, and double click the Workbook file name to open it in your InsMark System.

|

Note: If you are viewing this on a cell phone or tablet, the downloaded Workbook file won’t launch in your InsMark System. Please forward it to your PC where your InsMark System(s) are installed. |

For help on how to use InsMark software, go to The Quickest Way To Learn InsMark.

InsMark’s Referral Resources

(Put our Illustration Experts to Work for Your Practice)

We created Referral Resources to deliver a “do-it-for-me” illustration service in a way that makes sense for your practice. You can utilize your choice of insurance company, there is no commission split, and you don’t have to change any current relationships. They are very familiar with running InsMark software.

Please mention my name when you talk to a Referral Resource as they have promised to take special care of my readers. My only request is this: if a Referral Resource helps you get the sale, place at least that case through them; otherwise, you will be taking unfair advantage of their generous offer to InsMark licensees.

Save time and get results with any InsMark illustration. Contact:

- Ben Nevejans, President of LifePro Financial Services in San Diego, CA.

![]()

Testimonials

“The InsMark software is indispensable to my entire planning process because it enables me to show my clients that inaction has a price tag. I can’t afford to go without it!”

David McKnight, Author of The Power of Zero, InsMark Gold Power Producer®, Grafton, WI

“InsMark has increased my production by 10 fold. It clearly communicates to the client the best financial scenario to take.”

Gary Sipos, M.B.A., A.I.F.®, InsMark Platinum Power Producer®, Sipos Insurance Services, Freehold, NJ

“InsMark is the Picasso of the financial services world — their marketing savvy never fails to amaze me.”

Doug Peete, Past President, Top of the Table, and InsMark Power Producer, Overland Park, KS

“InsMark”, and the InsMark logo are registered trademarks of InsMark, Inc.

“InsMark Compare”, and “InsMark Prudent Care” are trademarks of InsMark, Inc.

Copyright © 2020 InsMark, Inc.

All Rights Reserved

Important Note #1: The hypothetical life insurance illustrations and alternative investments referred to in this Blog assume the nonguaranteed values shown continue in all years. This is not likely, and actual results may be more or less favorable. Actual illustrations of life insurance are not valid unless accompanied by a basic illustration from the issuing life insurance company.

Important Note #2: The information in this Blog is for educational purposes only. In all cases, the approval of a client’s legal and tax advisers must be secured regarding the implementation or modification of any planning technique as well as the applicability and consequences of new cases, rulings, or legislation upon existing or impending plans.

Important Note #3: Many of you are rightly concerned about the potential tax bomb in life insurance that can accidentally be triggered by a careless policyowner when policy loans are present and net cash values are so low that the income tax on the gain on surrender (calculated using gross cash values less basis) is more – often significantly more – than the net cash surrender value.

This lurking tax bomb can be present in all forms of whole life and universal life where policy loans of any type are utilized. It can be avoided, and you, the producer, are key to making sure your clients are aware of how to sidestep it.

A tax bomb can be avoided if the policy is neither surrendered nor allowed to lapse, since the policy death benefit wipes away the income tax liability. The foundation of this special treatment is IRC Section 101. This statute provides that the proceeds of life insurance maturing as a death claim are exempt from federal income tax. This applies to the full death benefit, including any cash value component whether loans exist or not.

Can your clients remember these facts years into the future? If they are incapacitated, will family members understand the issues? It is probably best to file a short note with the policy – something like this (although your compliance officer will likely have preferred language):

If/when you take policy loans on this policy, be sure to talk to your financial adviser before surrendering or lapsing the policy in order to anticipate unexpected tax consequences that may otherwise be avoided.

Some life insurance companies have concierge units that monitor loan status at the point of lapse or surrender, and you would be well-advised to select an insurance company with this capacity. To be effective regarding the tax bomb, such carriers need to be proactive in their client relationships, not merely reactive to client inquiries. I hope that ultimately the policyholder service division of all life insurance companies will bring this potential liability to the attention of those surrendering or lapsing policies, particularly those policies with 50% or more of the gross cash value subject to outstanding loans.

![]()

More Recent Blogs:

Blog #198 How Far Will $1,000,000 Go (Part 2) Joe and Annie Jordan’s Comprehensive Retirement Plan

Blog #197: How Far Does $1,000,000 Go (Part 1)

Blog #195: CheckMate® Logic (Part 3 of 4) Religion, Politics, Sex, and Term Insurance

Blog #194: CheckMate® Logic (Part 2 of 4) Measuring the Value of Permanent Life Insurance

| 3 Reasons Why It’s Profitable For You To Share These |

| Blog Posts With Your Business Associates and |

| Professional Study Groups (i.e. “LinkedIn”) |

Robert B. Ritter, Jr. Blog Archive