(Click here for Blog Archive)

(Click here for Blog Index)

(Presentations in this blog were created using the InsMark® Illustration System)

Suppose someone says to you:

- “Cash value life insurance is a rip-off only a financial idiot would buy.”

- Or “It’s better to buy term insurance and invest the difference.”

- Or “Why would you spend thousands for something you could get for a few hundred?”

- Or maybe you run into Suze Orman who says repeatedly:

“I HATE WHOLE LIFE INSURANCE”

“I HATE INDEXED UNIVERSAL LIFE INSURANCE”

“I HATE VARIABLE LIFE INSURANCE”

“THE ONLY TYPE I LIKE IS TERM INSURANCE.”

Words don’t count – only the mathematics, as you will see below.

There is no valid economic theory that explains why a bad idea is acceptable simply because one hears it frequently.

So – consider asking this question of those who think like Suze Orman, Dave Ramsey, or the White Coat Investor:

- If something important you believe to be true turns out to be wrong,

- when would you want to know about it?

How about . . . now?

Case Study

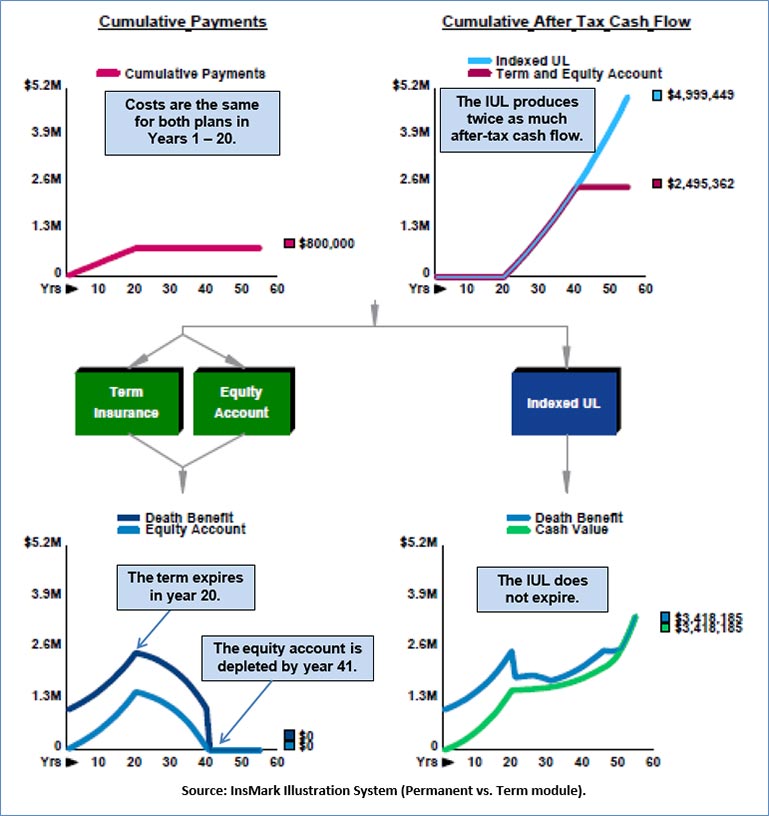

George Baker is age 45 and is in a 40% marginal tax bracket. He plans to purchase $1,000,000 of indexed universal life (IUL) with scheduled premiums of $40,000 a year for the first 20 years; $0 thereafter. Cash values are illustrated growing at 6.40%, and the policy provides:

- Protection for his family;

- After-tax participating loans of $100,000 a year indexed at 2.00% for a cost of living (COLA) adjustment from age 65 to 95. Including the COLA, loans for after-tax retirement cash flow total $4,999,449.

One of George’s advisers asks, “Why would you spend $40,000 when you could get term insurance for around $1,000?”

If that’s all there is to it, he shouldn’t. But has anyone ever bothered to show you mathematically why term insurance is the preferred choice? Or if you ask, do you get something like, “Duh . . . isn’t it obvious?”

It’s not obvious at all. American humorist Josh Billings once said that “It ain’t ignorance causes so much trouble; it’s folks knowing so much that ain’t so.”

We compared George’s IUL to $1,000,000 of 20-year term insurance at $1,030 a year (the lowest rate I could find). The term insurance alternative includes an equity account yielding 6.50% on $38,970 a year, the difference between the $40,000 premium for IUL and the $1,030 term premium. I include a dividend yield of 2.00% and a management fee of 0.50% for the equity account.

For the term insurance and equity account to match the IUL, the equity account has to deliver the same indexed cash flow of $4,999,449 over 30 years. It doesn’t come close to doing so. To match the IUL, the equity account would have to earn 9.20% – plus the 2.00% dividend – for a combined yield of 11.20%, 480 basis points more than the IUL.

| Image 1 |

| Term and an Equity Account |

| vs. |

| Indexed Universal Life |

Click here to review the comparison illustration in detail.

Conclusion

If cash flow is in short supply or the need for coverage is for a brief period, term insurance can make sense. However, for longer intervals, if the cash flow exists to buy what you want, a cash value policy is the only logical choice.

Remember: Words don’t count – only the mathematics.

Licensing

To license the InsMark Illustration System, contact Julie Nayeri at julien@insmark.com or 888-InsMark (467-6275) or visit us online. Institutional inquiries should be directed to David Grant, Senior Vice President – Sales, at dag@insmark.com or (925) 543-0513.

Your Comments

What are your thoughts, conclusions, or questions after reviewing this material? Please add your comments to this Blog.

Creating Similar Presentations

If you would like highly qualified design assistance with no commission split required, contact LifePro Financial, InsMark’s Referral Resource discussed below.

The video below can also acquaint you with the general subject of downloading and using InsMark’s Digital Workbook Files.

Digital Workbook File for Blog #209

InsMark Illustration System

Assuming you are licensed for the InsMark Illustration System, you can download the same Digital Workbook File below that I used to prepare the Case Study for this Blog.

|

Before downloading and reviewing any files, be certain you have installed the most current updates to your InsMark System(s). Do this using Live Update available under Help on the main menu bar of the System or this icon on the main menu bar:

Note: If you are viewing this on a cell phone or tablet, the downloaded Workbook file won’t launch in your InsMark Systems. Please forward the Workbook where you can launch it on your PC where your InsMark System(s) are installed. |

InsMark’s Referral Resources

(Put our Illustration Experts to Work for Your Practice)

We created Referral Resources to deliver a “do-it-for-me” illustration service in a way that makes sense for your practice. You can utilize your choice of insurance company, there is no commission split, and you don’t have to change any current relationships. They are very familiar with running InsMark software.

Please mention my name when you talk to a Referral Resource as they have promised to take special care of my readers. My only request is this: if a Referral Resource helps you get the sale, place at least that case through them; otherwise, you will be taking unfair advantage of their generous offer to InsMark licensees.

Save time and get results with any InsMark illustration. Contact:

- Ben Nevejans, President of LifePro Financial Services in San Diego, CA.

“InsMark” and the InsMark logo are registered trademarks of InsMark, Inc.

© Copyright 2021, InsMark, Inc.

All Rights Reserved

Important Note #1: The hypothetical values associated with this Blog assume the nonguaranteed values shown continue in all years. This is not likely, and actual results may be more or less favorable. Life insurance illustrations are not valid unless accompanied by a basic illustration from the issuing life insurance company.

Important Note #2: Many of you are rightly concerned about the potential tax bomb in life insurance that a careless policyowner can accidentally trigger. This is mainly a problem when policy loans are present, and net cash values are so low that the income tax on the gain on surrender (calculated using gross cash values less basis) is significantly more than the net cash surrender value.

This lurking tax bomb can be present in all forms of whole life and universal life where policy loans of any type are utilized. It can be avoided, and you, the producer, are key to making sure your clients are aware of how to sidestep it.

A tax bomb can be avoided if the policy is neither surrendered nor allowed to lapse, since the policy death benefit wipes away the income tax liability. The foundation of this special treatment is IRC Section 101. This statute provides that the proceeds of life insurance maturing as a death claim are exempt from federal income tax. This applies to the full death benefit, including any cash value component whether loans exist or not.

Note: It is best if you design the policy with no premiums scheduled after retirement if loans are anticipated in retirement years. This may require higher premiums during pre-retirement years, but a policy with no premiums scheduled is much more tolerable at advanced ages than one with continuous premiums.

Can your clients remember these facts years into the future? If they are incapacitated, will family members understand the issues? It is probably best to file a short note with the policy – something like this (although your compliance officer will likely have preferred language):

If/when you take policy loans on this policy, be sure to talk to your financial adviser before surrendering or lapsing the policy in order to anticipate unexpected tax consequences that may otherwise be avoided.

Does this note make it harder or easier to deliver the policy? It’s harder if you haven’t discussed it with your client; easier if you have. And that’s the point – you should discuss it.

Some life insurance companies have concierge units that monitor loan status at the point of lapse or surrender, and you would be well-advised to select an insurance company with this capacity. To be effective regarding the tax bomb, such carriers need to be proactive in their client relationships, not merely reactive to client inquiries. I hope that ultimately the policyholder service division of all life insurance companies will bring this potential liability to the attention of those surrendering or lapsing policies, particularly those policies with 50% or more of the gross cash value subject to outstanding loans.

![]()

More Recent Blogs:

Blog #208: Dollars to Charity for Pennies of Cost

Blog #207: Merry Christmas and Happy Holidays from InsMark

Blog #205: Escaping an Oncoming Financial Nightmare

Blog #204: Leveraged Executive Bonus (Part 2 of 2)

| 3 Reasons Why It’s Profitable For You To Share These |

| Blog Posts With Your Business Associates and |

| Professional Study Groups (i.e. “LinkedIn”) |

Robert B. Ritter, Jr. Blog Archive